Surgery as a Career in 2026: Salary, Demand & Risk Outlook

Max Schloemann2026-02-27T19:41:22+00:00Surgery remains one of the most demanding and rewarding career paths in medicine. In 2026, the field is evolving fast as the population ages, technology advances, and reimbursement and regulatory pressures reshape practice.

Demand for surgical care is rising, and many specialties remain among the highest-paid in healthcare. But the path comes with real tradeoffs, including intense training, workload strain, and increased malpractice risk.

This article breaks down the surgical career outlook in 2026, including demand, compensation, emerging technologies, and the key opportunities and risks surgeons should understand.

Table of Contents

What Do Surgeons Do?

Surgeons are physicians trained to diagnose conditions that require operative treatment and to perform procedures that restore function, relieve pain, and save lives. While the public often associates surgery with the operating room, a surgeon’s responsibilities extend well beyond the procedure itself.

Surgeons are involved in every phase of patient care, including:

Where Do Surgeons Work?

According to the American College of Surgeons, standard workplace settings for a surgeon include:

- Hospitals

- Academic Medicine

- Private Practice

- Ambulatory Surgery Centers

- Contract Assignments Through Staffing Agencies

- Institutional Practice

- Government Service Programs

- Military/Uniformed Services

Professional Advantages for Surgeons in 2026

The following factors contribute to a favorable outlook for surgeons in 2026 and beyond:

- Growing Market Value in the U.S.

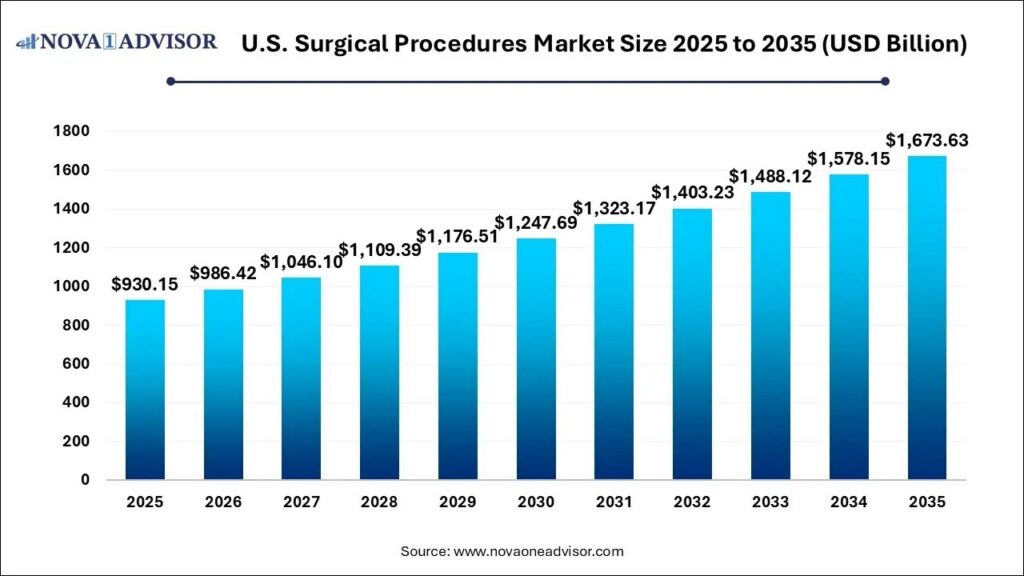

The U.S. Surgical Procedures Market measured $930 billion in 2025 and is expected to reach around $1.67 trillion by 2035.

These market growth predictions indicate that surgeons will experience considerable flexibility and autonomy with employment opportunities.

U.S. Surgical Procedures Market Size (2025-2035)

Surgical procedures in the United States are expected to reach a market value of $986 billion in 2026 and $1.67 trillion by 2035.

Source: Nova One Advisor

- Increasing Demand for Surgery

According to the U.S. Bureau of Labor Statistics, physician and surgeon employment is projected to grow 3% between 2024 and 2034, with 23,600 openings projected each year during that time.

| Specialty | Employment, 2024 | Projected Employment, 2034 | Projected Growth, 2024-2034 |

|---|---|---|---|

| All physicians & surgeons | 839,000 | 863,200 | 3% |

| Ophthalmologists, except pediatric | 12,500 | 13,100 | 4% |

| Orthopedic surgeons, except pediatric | 14,700 | 15,300 | 4% |

| Pediatric surgeons | 1,100 | 1,100 | 2% |

| Surgeons, all other | 25,100 | 26,100 | 4% |

The projected growth rate varies across specialties, with most surgical specialties expected to grow at rates above the 3% physician/surgeon average.

Source: U.S. Bureau of Labor Statistics

- Several factors are driving increased demand for surgical specialists in the United States. One of the most significant is the aging Baby Boomer population, which increases surgical demand while also contributing to workforce shortages.

- Aging General Population

According to the World Health Organization, the world’s population aged 60 or older will double by 2050. An older population typically requires more surgical interventions, including orthopedic hip and knee replacements, interventional cardiology, and cataract surgeries. This explains why ophthalmologists’ and pediatricians’ employment projections have the highest and lowest expected growth rates, respectively.

-

- Aging Surgical Workforce

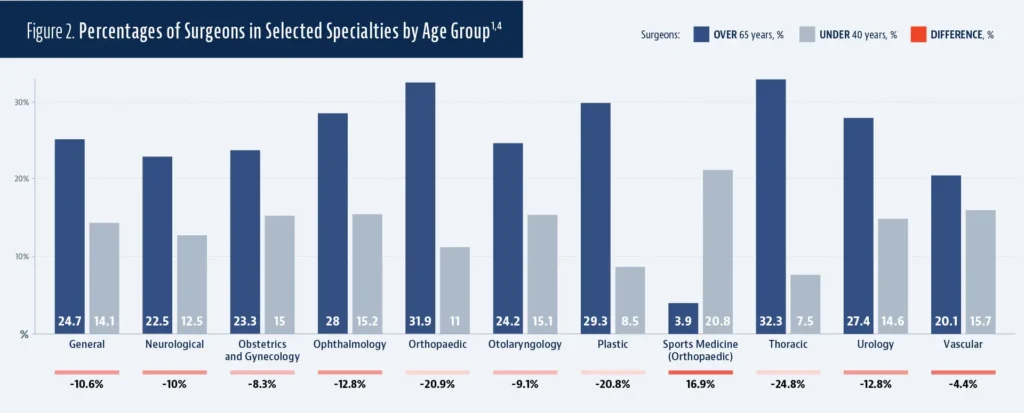

At the end of 2022, 25.6% of surgeons were older than 65 years. That percentage was even higher for the subspecialties of ophthalmology, orthopedics, plastic surgery, thoracic surgery, and urology.As more Baby Boomer surgeons reach retirement age, the Association of American Medical Colleges (AAMC) projects that the U.S. will face a physician shortage of up to 86,000 providers by 2036.This impending gap signifies ample growth opportunities for new surgeons entering the field and a potential avenue for experienced surgeons to advance into leadership roles.

- Aging Surgical Workforce

-

Expanded Patient Access

As telemedicine becomes more widely available and accepted, surgeons can offer remote patient consultations to a broader population, and multidisciplinary specialist teams can collaborate virtually to help patients anywhere in the country.

To further improve healthcare accessibility, some local governments and healthcare organizations offer incentives – such as scholarships, loan forgiveness, and stipend programs – to attract and retain surgeons in underserved regions.

- Groundbreaking Innovations

Why is the Demand for Surgeons Increasing?

Key contributing factors to surgeon demand:

-

-

-

Robotic Surgery

Robotic systems, such as the widely popular da Vinci surgical system, enable smaller incisions, greater precision, and faster patient recovery times.

-

Artificial Intelligence

AI can improve surgical efficiency and patient safety by assisting surgeons with preoperative planning, imaging, and real-time analytics, as well as navigation during an operation.

-

Virtual & Augmented Reality (VR & AR)

VR simulators create a realistic training environment for surgeons that poses zero risk to human patients. Studies have shown that VR training can improve procedural accuracy compared to traditional methods, leading to better patient outcomes and reduced liability risk for the surgeon.

In the operating room, AR overlays of patient data and 3D anatomical models can be projected directly onto the surgery site, helping surgeons make accurate, data-driven decisions in real time.

-

-

- High Earning Potential

According to the Medscape Physician Compensation Report 2024, surgeons remain among the highest-paid healthcare providers due to their specialized skills and high level of responsibility.

Average Annual Earnings for U.S. Physicians & Surgeons

Surgical specialties rank among the top-paid specialists in average annual earnings.

Source: 2024 Medscape Physician Compensation Report

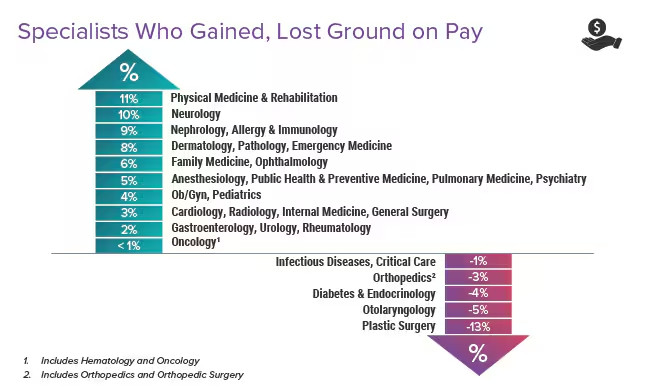

Change in Physician & Surgeon Pay by Specialty

Specialist compensation changes ranged from +11% to -13%, with some surgical specialities experiencing salary growth and others declining.

Source: 2024 Medscape Physician Compensation Report

Professional Challenges for Surgeons in 2026

In 2026, surgeons will likely face obstacles related to industry trends, regulatory changes, and malpractice litigation precedents.

- Rigorous Commitment

Obtaining the necessary education, training, and credentials to become a surgeon requires significant time commitments and substantial financial investment.

Education & Training Requirements to Practice Surgery Independently

A commitment of this length and vigor requires personal sacrifice, often at the cost of work-life balance during the most intense phases. However, emerging trends such as mentorship programs, loan forgiveness policies, and VR-assisted training programs show promise for revolutionizing the process.

- Disruptive Regulatory Changes

State and federal regulatory policies focusing on patient safety, quality of care, and financial reimbursement are influencing surgical practice in a variety of ways, such as:

-

- Value-Based Care Payment Model

As the fee-for-service model shifts to a value-based care model that links compensation to quality over quantity, surgeons are held more accountable for their care.January 1, 2026, TEAM (Transforming Episode Accountability Model), a new value-based model that impacts payments for Medicare patients undergoing certain surgeries, became mandatory in 188 geographic regions.

- Value-Based Care Payment Model

-

- Reproductive Care

For OB/GYN surgeons specifically, abortion legislation complicates patient care and liability exposure depending on their location. OB/GYNs must navigate a complex and evolving situation to minimize professional liability while delivering safe, compliant care to pregnant women.Abortion legislation also impacts provider shortages. According to a March of Dimes report, states where abortion is prohibited have fewer OB/GYNs per 10,000 births compared to states where abortion is less regulated. As of July 2025, 52% of U.S. counties lacked a single hospital with obstetric care.

OB/GYNs in less-regulated states could see an increase in out-of-state and remote patients, which requires careful attention to state legal requirements and malpractice coverage parameters.

- Reproductive Care

-

- 2026 Medicare Reimbursement Adjustments

After years of Medicare pay cuts, the 2026 Medicare Physician Fee Schedule includes a 2.5% increase effective January 1, 2026. However, that increase is largely offset by other cuts, including a 2.5% efficiency adjustment affecting nearly 91% of physician services. This cut will significantly reduce—or even eliminate—net gains for many practices.

- 2026 Medicare Reimbursement Adjustments

- High-Risk, High-Liability Field

The medical malpractice statistics of 2024 demonstrate the high liability landscape for surgeons:

-

- Surgical errors account for 25% of all negligent provider claims.

- Surgeons are most likely to be sued for malpractice.

- High-risk specialties are most vulnerable to medical malpractice claims and lawsuits, including:

- OB/GYNs

- General Surgeons

- Orthopedic Surgeons

- Neurosurgeons

- Bariatric Surgeons

- Plastic Surgeons

- Ophthalmologists

- Otolaryngologists

- Urologists

Malpractice insurance premiums are expected to keep climbing in 2026.

Projected rate increases reflect the substantial risks of surgery and recent escalations in legal defense fees, social inflation, and nuclear payouts.

“Nuclear verdicts continue to increase at a drastic rate: The average of the top 50 medical malpractice verdicts was $32 million in 2022, $48 million in 2023, and an alarming $56 million in 2024.”

-The Doctors Company

Safeguard Your Career with Premier Liability Coverage

SURGPLI brokers specialize in finding affordable, robust coverage for surgeons in high-risk specialties who are often targets for medical malpractice lawsuits.

With strong malpractice insurance coverage, surgeons can focus on helping patients without worrying about professional liability exposure.

Surgery Career FAQs

Contact us for a free evaluation or TAIL INSURANCE quote

Read the latest From SURGPLI

Medical malpractice expert Max Schloemann breaks down surgeon salary, demand & risk trends in 2026—plus key career advantages & challenges. Read here.

Medical malpractice insurance specialist Max Schloemann recommends the top liability insurance companies for doctors in 2025. Learn how to compare carriers here.

Read key information Texas OB/GYN surgeons need to know about medical malpractice insurance. State laws, types of insurance, cost factors & more. Get a quote here.

Stay In Touch